Special-Needs Trusts: How They Work and What Has Changed

Trusts give parents of special-needs children additional options for extending care and financial assistance. But you might need some expert help.

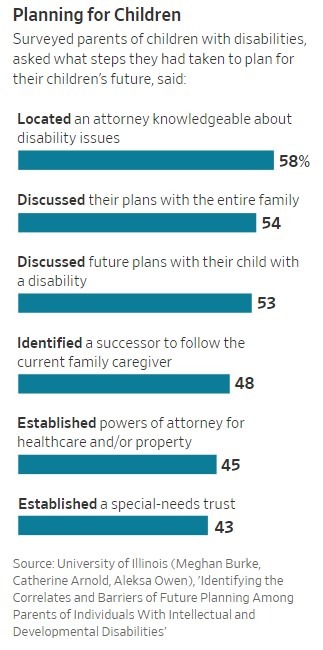

Many parents aren’t sure where to start when it comes to financial planning for children with special needs.

ILLUSTRATION: JOÃO FAZENDA

Can you explain how a special-needs trust works? We have an adult child on disability and have been told we can set up a special-needs trust for her. We have an individual retirement account that we could assign to the trust, but we aren’t sure what the tax requirements are or if there has to be a required minimum distribution.

Good questions. Special-needs trusts have been around for a number of years, but two parts of this picture are changing.

First, many people with disabilities and chronic illnesses, thanks to advances in medicine, are living longer lives—and, as such, are outliving their parents and primary caregivers. That makes the need for long-term planning all the more vital.

Second, recent changes in tax laws—and, in particular, the rules governing inherited retirement accounts—mean that families, at the least, should review their financial plans as they apply to children with special needs.

Such planning, of course, has never been easy. The unknowns are unsettling (how much care will be needed, at what cost, and for how long?); tax rules are complex; fees can be steep; and whatever decisions are made, frequently, must fit within a larger estate plan that involves other family members.

Indeed, many parents aren’t sure where to start. A University of Illinois study in 2018 found that less than half of parents of children with disabilities are planning for their children’s future. It wasn’t a matter of negligence; rather, parents told researchers that they were simply overwhelmed—by, among other issues, stress, lack of time (days were filled with caregiving duties) and a reluctance among family members to help.

With this in mind, here are some fundamentals:

At its simplest, a special-needs trust “is set up to protect the assets of a person with a disability or other medical conditions,” says Mindy Neira, a certified financial planner with Modera Wealth Management in Westwood, N.J., who specializes in this area. For instance, parents who have a child with autism could create and fund such a trust. The trust, in turn, could help pay for various goods and services for the child: medical equipment, education, home furnishings, etc.

Two features set a special-needs trust apart. First, a trustee is appointed to manage any and all spending; the beneficiary has no control over the assets inside the trust. Second, the fact that the assets aren’t owned outright by the beneficiary means that he or she remains eligible for government programs that place limits on assets, such as Supplemental Security Income (managed by the Social Security Administration) or Medicaid.

There are several types of special-needs trusts, including pooled, first party and third party. Not surprisingly, Mrs. Neira says, these vehicles—given their unique language, how they are funded and the tax consequences—can be difficult to assemble. As such, it’s wise to get some expert help.

A good book to begin educating yourself is “Special Needs Trusts: Protect Your Child’s Financial Future,” by Kevin Urbatsch and Michele Fuller-Urbatsch. Next, seek out a chartered special-needs consultant, or ChSNC. Financial advisers and others with this designation and training typically are better able to help families navigate these waters. The American College of Financial Services has a tool that can help people find a ChSNC in their area. Go to youradvisorguide.com and click on Browse Advisors.

In addition, there are lawyers who focus on special-needs trusts and drafting these documents. You can find a directory of such individuals at Special Needs Alliance (specialneedsalliance.org).

As for your question about your IRA, the short answer is: You can’t “assign” an IRA to a special-needs trust, says Ed Slott, an IRA expert in Rockville Centre, N.Y. But you can name a special-needs trust as a beneficiary of your IRA. In this way, after you die, withdrawals from the retirement account will be paid to the trust for the benefit of your child.

And yes, required minimum distributions (RMDs) would come into play. That’s because your IRA, after you die, would become an “inherited IRA,” and your special-needs trust (if named as the IRA beneficiary) would be required to take distributions from the account.

But here, your child could catch a break.

As you might recall, the Secure Act, enacted in 2019, ended the so-called stretch IRA for many heirs. An adult child, for instance, who inherits an IRA from a parent is now required to withdraw all of the money from the account—and pay any taxes due—within a decade of the parent’s death.

But the Secure Act, Mr. Slott notes, also identified several groups of heirs who still can stretch required distributions over their lifetimes, including individuals who are “disabled” or “chronically ill.” If, before you die, you set up a special-needs trust with your disabled child as the beneficiary—and if you name that trust as the beneficiary of your IRA—this would allow the trust to withdraw funds from the IRA over the life expectancy of your child. In effect, you restore the stretch IRA.

(To be specific, to take advantage of the stretch IRA, your trust would need to qualify as an “applicable multi-beneficiary trust,” which Congress created as part of the Secure Act. We don’t have room here to tackle this type of trust in detail, but listen for this term if you get serious about drafting a special-needs trust.)

Two final and important points. First, much of the above assumes that, at the time of your death, your child is, in fact, “disabled” or “chronically ill” as set out in the tax code. And that might not be the case. Both terms are defined “restrictively, to say the least,” Mr. Slott notes; as such, “qualifying for either disabled or chronically ill status is no easy hurdle.” (Search online, respectively, for: tax code section 72(m)(7) and tax code section 7702B(c)(2).) Your adult child likely will need a doctor’s certification.

Second, ask yourself and, ideally, your financial adviser: Is a traditional IRA the best way to fund a special-needs trust? Yes, an IRA is where people have most of their savings. But a large IRA can mean large required distributions. If the trust ends up retaining some of those distributions to ensure that your child doesn’t lose her eligibility for government support, the trust itself could end up with some big tax bills, Mr. Slott says. (Yes, trusts, in some cases, are subject to taxes.)

Two, possibly better, solutions: Roth IRAs and life insurance. With the former, required distributions, whether they are paid out to your child or retained in the trust, would be income tax-free, Mr. Slott says. With the latter, there are no required distributions and, thus, fewer tax land mines.

“Generally, the better move,” Mr. Slott says, “is to exchange assets like traditional IRAs for more tax-efficient assets like Roth IRAs and life insurance to accomplish the post-death planning objectives that people are looking for.”

Get your complimentary download here:

source article: https://www.wsj.com/articles/special-needs-trusts-how-they-work-and-what-has-changed-11622743200