How to Avoid a Tax Bomb When Selling Your Home

- Single filers may exclude up to $250,000 of capital gains on home sales profits, while married couples may subtract up to $500,000.

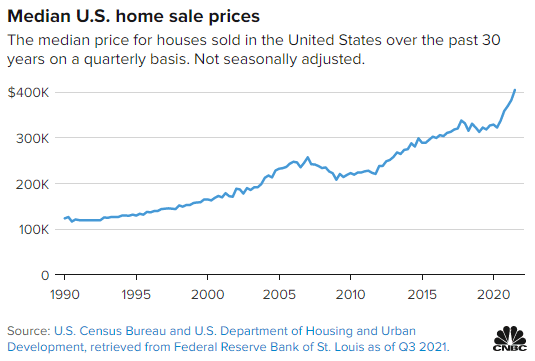

- However, median home sales prices have more than doubled over the past two decades, pushing some long-term homeowners over the thresholds.

- Sellers may lessen the tax bite by reducing profits with past home improvements, among other tactics, experts say.

![]()

With soaring home values, many sellers expect a sizable profit when listing their property. However, capital gains taxes may put a damper on their windfall.

Home sales profits are considered capital gains, taxed at federal rates of 0%, 15% or 20% in 2021, depending on income.

The IRS offers a write-off for homeowners, allowing single filers to exclude up to $250,000 of profit and married couples filing together can subtract up to $500,000.

But these thresholds haven’t changed since 1997, and median home sales prices have more than doubled over the past two decades, affecting many long-term homeowners.

“It’s become a huge part of the conversation now,” said John Schultz, a CPA and partner at Genske, Mulder & Company in Ontario, California.

While the exemption may be significant for some homeowners, there are strict guidelines to qualify. Sellers must own and use the home as their primary residence for two of the five years preceding the sale.

“But the two years don’t have to be consecutive,” said Mary Geong, a Piedmont, California-based CPA and enrolled agent at the firm in her name.

Someone owning two homes may split time between the properties, and if their cumulative time living at one place equals at least two years, they may qualify.

Moreover, someone may convert a rental property to a primary residence for two years for a partial exclusion. In that case, the write-off is based on the percentage of their time spent living there, she explained.

For example, home additions, patios, landscaping, swimming pools, new systems and more may qualify as improvements, according to the IRS.

“But you need good recordkeeping,” Geong added.

Increase basis to reduce profits

If homeowners exceed the exemptions and owe taxes, they may reduce profits by adding certain home improvements to the original purchase price, known as basis, Schultz explained.

For example, home additions, patios, landscaping, swimming pools, new systems and more may qualify as improvements, according to the IRS.

However, ongoing repairs and maintenance expenses that don’t add value or prolong the home’s life, such as painting or fixing leaks, won’t count.

Of course, homeowners need to show proof of improvements, which can be difficult after many years. However, if someone lost receipts, there may be other methods.

“Property tax history can help you go back and recalculate some of that,” Schultz pointed out, explaining how reasonable estimates may be acceptable.

Homeowners may also increase basis by adding certain closing costs, such as title, legal or surveying fees, along with title insurance.

Other tax consequences

There’s also the possibility of other tax consequences when selling a home with a large profit.

For example, boosting adjusted gross income can affect eligibility for health insurance subsidies, and may require someone to pay back premium credits at tax time.

And retirees increasing income may trigger higher future payments for Medicare Part B and Part D premiums.

“If you’re selling any asset of significance, you should be talking to some type of advisor,” Schultz said.

A financial advisor or tax professional can project possible outcomes depending on someone’s complete situation to help them pick the best move.

Enjoy this complimentary download:

By submitting your contact information, you consent to be contacted regarding retirement income strategies that utilize investments and insurance products.

Source Article: https://www.cnbc.com/2021/12/02/how-to-avoid-a-tax-bomb-when-selling-your-home.html